By Innocent Ephraim, Contributing Writer

Instant or real-time payments will become part of daily life in the not-too-distant future. Across the world, governments and financial institutions are putting significant efforts into bringing affordable and safe instant payments systems to market. This seemingly simple payments system is actually quite complex. Nonetheless, since 2016, many countries across the world and the African region are seeing the overriding benefits of leapfrogging longstanding barriers in pursuit of greater financial inclusion and economic growth.

Using technology to change the landscape of the financial sector

Instant payment systems are transforming the financial landscape across the world, offering both short term and long-term economic benefits. Governments and banking institutions are under increasing pressure from consumers and businesses to provide real-time payment services to maximise the opportunities offered by digital financial services and achieve competitive advantage in the fast pace of change within the Fourth Industrial Revolution.

“The Fourth Industrial Revolution, finally, will change not only what we do but also who we are. It will affect our identity and all the issues associated with it: our sense of privacy, our notions of ownership, our consumption patterns, the time we devote to work and leisure, and how we develop our careers, cultivate our skills, meet people, and nurture relationships.”

Klaus Schwab, The Fourth Industrial Revolution

Characterised by a fusion of technologies that blurs the lines between the physical, digital, and biological spheres, the impact of the Fourth Industrial Revolution is significant, not only on the type of financial systems in the market, but also their speed and scope. Over a decade ago, the evolution of digital financial services made an unprecedented impact on financial inclusion, providing broad distribution channels and inclusive access for millions of people around the world, reducing cash dependency, introducing new and more seamless services in the market and facilitating domestic and international money transfers.

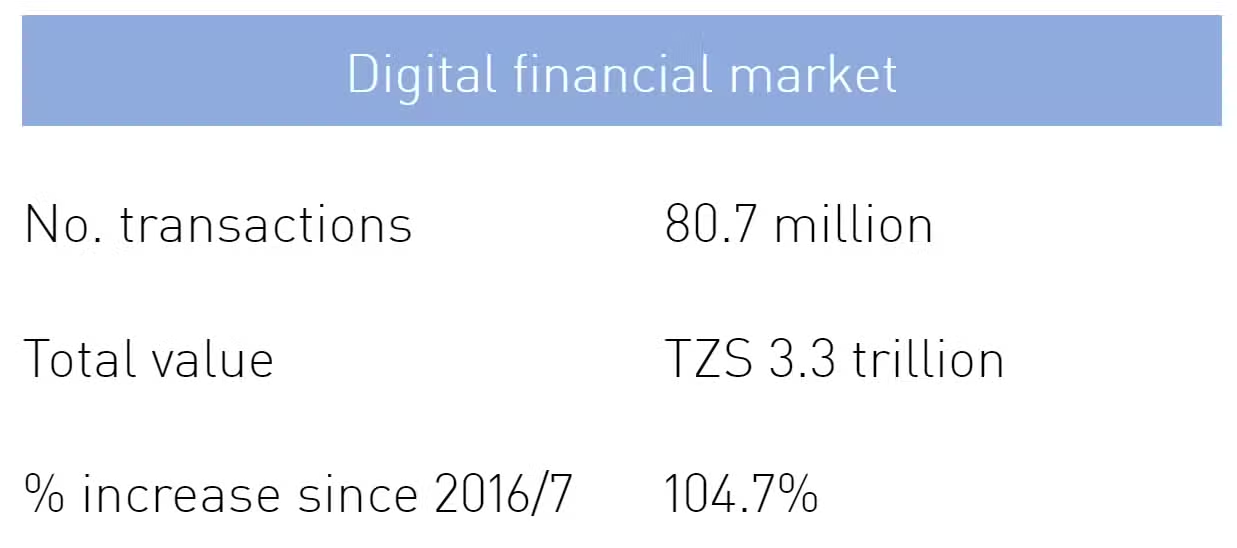

State of digital financial service sector in Tanzania

Tanzania’s achievements in expediting innovative digital financial services across the country and their considerable impact on financial inclusion are now well known and documented worldwide. Over the past year, mobile money transactions have continued to grow and now stand at over 80 million with a total value of over TZS 3 trillion. Such success has become a prime example of the level of growth in access, uptake and usage of financial services that can be attained when appropriate innovative technologies, enabling policies and cooperative stakeholders work in tandem.

It is now common to see services such as utility bill payment, payroll distribution, and point-of-sale purchases being offered through digital financial services platforms. All of these accessible through six mobile money issuers and over 37 commercial banks.

Benefits of instant payment systems

Like in many countries worldwide, despite the success of digital financial services, the current payment system in Tanzania presents considerable challenges across the market.

Service providers face many challenges from the current interoperability model utilised in the country, including dependency on bilateral agreements, high investment, maintenance and transaction costs and poor liquidity management, scalability and interchanging. An instant payment system would provide a fast, integrated and cost-efficient clearing and settlement platform which could not only reduce costs but also increase commercial opportunities and address unmet market demands.

For customers, the introduction of the real-time payments will allow transactions at any time, irrespective of provider, helping to make payments more affordable and faster, thus encouraging greater use of electronic payments.

For the Bank of Tanzania, the current system presents many regulatory challenges in terms of oversight due to limited visibility of transactions. An integrated instant payment system could support improved efficiencies in governance, safety, consumer protection and risk management for both payment service providers and end-users, as well as enhanced tax collection processes.

For all stakeholders across the financial sector in Tanzania, the opportunities presented by an instant payment system will no doubt improve the speed and scope of the financial services which are currently offered, but also revolutionise policies and product development to realise innovative, allowing Fintechs and start-ups to build on top of the current rails as customer value is enhanced, this enables the FSPs to focus on their strengths.

Driven by the principles of the Tanzania instant payment system which state, the design principles for the TIPS scheme and are described below:

Rationale & Implications

Open and Interoperable

The system is open for use by all licensed Digital Financial Services Providers (DFSPs) in the country, including banks, eMoney issuers and aggregators.

An open system will allow any payer to reach any payee; it will also encourage competition by enabling multiple providers to reach other DFSPs.

“Push” (Credit Transfer) Payments

Payment orders are submitted to the switch only by the payer’s DFSP.

Eliminates risks and costs inherent in “pull” payments. Requires the use of “request to pay” messaging to enable certain merchant and bill pay use cases.

Real-time Payments

Payer and payee accounts are debited and credited instantly, and sender and receiver are notified immediately; system is available 365x7x24.

Meets expectations set by end users and made possible via modern technology.

All Use Cases

A single switch used for all retail use cases (consumers, businesses/merchants, and government), including P2P, P2B, P2G, G2P, B2P, B2G, B2B, G2B and CI/CO.

A single switch eliminates complexities and costs inherent in multiple switch scenarios; it also concentrates volume to enable low transaction costs. Note that all use cases will not be enabled at the first implementation of TIPS.

Irrevocable Payments

Payment orders cannot be rescinded once they reach the switch, providing assurance that the receiver’s account cannot be debited without their consent.

Same-day Settlement

The financial obligations among the DFSPs are settled within the day of payment execution, possibly with multiple settlement periods within the day.

Ultra-Low-Cost

Use of the switch is very low-cost for the participating DFSPs.

Price Transparency

All fees and taxes charged to payer will be displayed prior to transaction execution; the information exchange is enabled by the switch.

Payment Addressing

The switch has a capability that enables aliases for payments addressing.

Inclusive Governance

DFSPs have the opportunity to participate in the determination of the operating rules of the scheme.

DFSP participation in the rules contributes to a fair system, with no category of DFSPs having an advantage over the other.

Fraud Utility

The switch connects to a fraud management utility for the detection and management of certain types of fraud.

Connectivity to other Schemes

The switch is designed to connect with other payment systems and schemes to enable ease of transacting between and among schemes. This includes the ability to connect as needed to similar systems in other countries to effect cross-border remittances.

Regulatory Oversight

The scheme will enable regulators to monitor transactions for all DFSPs in real-time or near real-time.